Maersk acquires Hamburg Süd

The end of 80 years of family business

The ocean freight industry’s downturn has claimed its latest victim: Family-owned Hamburg Süd.

After weeks of speculation, the company confirmed its sale to Maersk on December 1st, 2016. Falling into the safe hands of the world’s largest shipping carrier, it marks the end of 80 years of family business for the German line.

Hamburg Süd

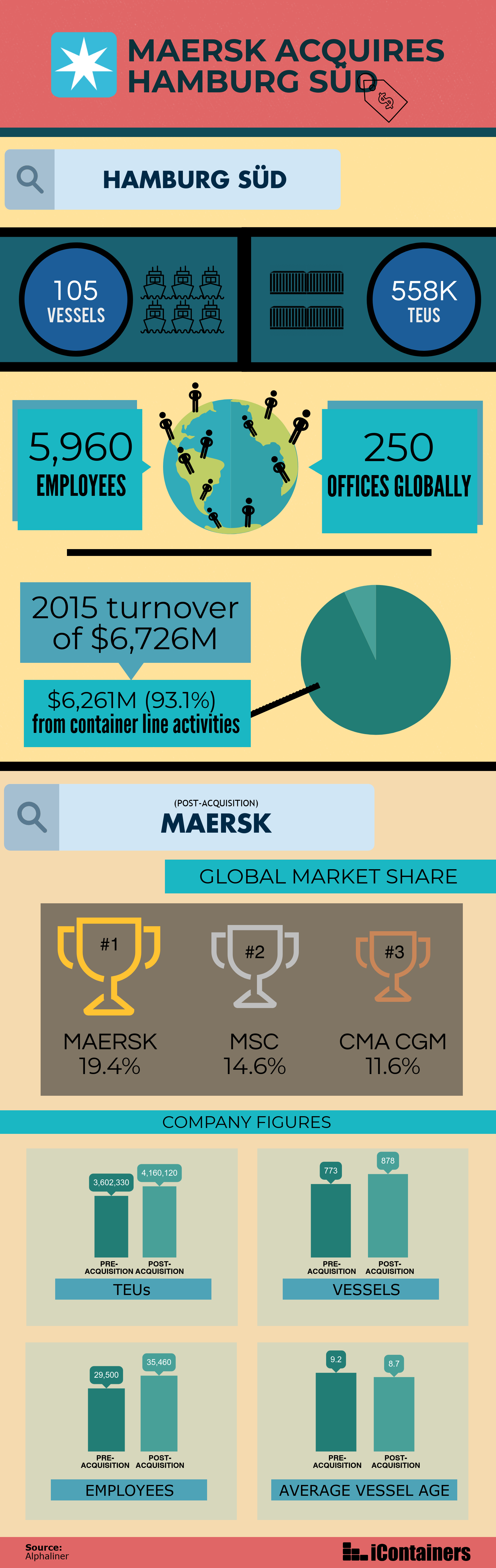

Headquartered in Hamburg, the German container line is fully owned by the Oekter Group. It holds the position of the world’s seventh-largest container line - a position previously held by Hanjin Shipping. While it does not have a large presence on the East-West routes, it is widely considered to be the leader in North-South trades. That’s largely thanks to its Hamburg Süd, CCNI and Aliança brands based in Chile and Brazil respectively.

“This is a move that makes sense. Hamburg Süd is the North-South lane where Maersk had all but pulled out a few years back before the re-launch of Sealand. Adding Hamburg Süd makes complete sense to make them the market leader in this trade as well.

On the Australia lane, Hamburg Süd and Maersk have traditionally been the premiere options. So they are taking over a key competitor in that market. Customers looking for a fast and reliable transit to Australia would usually look at either of the two first before looking at other carriers.”

– Klaus Lysdal, VP Sales & Operations, iContainers

Against the tide

Despite the global downturn, Hamburg Süd has done comparatively well. In 2015, the carrier recorded a turnover of $6.726 billion, of which $6.261 billion was generated from its container line activities.

“Global container liner shipping has been generating losses for years in the face of rising overcapacity. Nevertheless, Hamburg Süd has performed well compared with its competitors. It has grown clearly in excess of the market and has financed the expansion of its network as well as the ship and container fleet largely from its own cash flow.”

– Oetker Group statement

But even a fairy-tale must come to an end. The industry downturn has resulted in growing friction among family members over their maritime investment, prompting the idea to sell.

“Giving up our engagement in shipping after an 80 year-long ownership in Hamburg Süd was not an easy decision for my family. We are very confident, though, to have chosen the best of all possible partners.”

– August Oetker, chairman of Advisory Board of Dr. August Oetker KG, management holding company of Oetker Group

What the deal means

The confirmation follows weeks of sale speculation for the German family. French operator CMA CGM was even thrown in the mix even as recently as late November 2016.

With this purchase, Maersk cements its status as the world’s biggest container shipping line. According to industry analyst Alphaliner, Maersk’s global market share will increase to 19.4% from its current 16.8%. That further increases its gap from second-placed MSC, which holds a 14.6% market share.

Here’s a breakdown of the numbers and figures behind the acquisition.

Approvals obtained*

*Updated Dec 1, 2017

The acquisition finalized a year after the initial announcement, following regulatory approvals in the 23 jurisdictions needed. The latest and final stamp was given by the Korea Fair Trade Commission earlier this week. Regulatory approvals from China, Brazil, the US and the EU had already been obtained previously.

The price tag of the acquisition has been placed at $4.4 billion. For now, Maersk plans to keep Hamburg Süd as a separate entity. According to both parties, they expect to bring in operational synergies valued at around $350 million to $400 million annually from 2019 onwards.

“Hamburg Süd is a very well-run and highly respected company with strong brands, dedicated employees and loyal customers. Hamburg Süd complements Maersk Line and together we can offer our customers the best of two worlds, first of all in the North–South trades.”

Latest in a string of M&As

This is Maersk’s latest move indicating its refocus to acquisitions instead of ordering new ships. The company’s previous container line acquisition was 11 years ago in 2005 when it bought over P&O Nedlloyd.

“We have a healthy respect for the Hamburg Süd customer base so we will do our best to retain that and grow that customer base.”

– Robbert van Trooijen, Asia-Pacific Chief, Maersk Line

As a result of overcapacity and a prolonged period of low demand, the shipping industry has generated losses for years on end. That has resulted in a string of acquisitions and mergers among the industry’s biggest players.

“As a customer or consumer, the advantages include more services and initially better rates from the synergies created. But the concerns will be for how long. How long before rates start to go up? And what will one less player in the market mean to the declining customer service and quality levels we have seen from the carriers in recent years?”

– Klaus Lysdal, VP Sales & Operations, iContainers

2016 saw significant movements in the shipping industry. Just this year alone, CMA CGM acquired NOL, which includes the APL brand. UASC joined forces with Hapag-Lloyd, COSCO and China Shipping merged, and Japan’s big three conglomerates NYK, MOL and K-Line embarked on a joint venture.

All hoping to avoid the same fate as Hanjin Shipping.

Related Articles

Trump Tariff Tracker: A Comprehensive Timeline of U.S. Trade Policy in 2026